Insights

Want these insights and updates straight to your inbox? Subscribe to our monthly newsletter.

CHECK OUT OUR CLIMATE IMPACT REPORTS:

You Can’t Spell AI Without Borrowing Two Letters From CLIMATE

What does it mean to “make Partner”? Venture capital firms, like law and accounting firms, have a Partner track. It’s a level that ambitious team members aspire to, reflecting hard work, shared values and

An astounding two-thirds of all venture capital now flows into AI. But AI doesn’t exist in a vacuum. It runs on data centers and data centers run on energy—a lot of it. Meeting that demand by burning more fossil fuels is neither feasible nor economical. The only scalable path forward is continued renewable deployment, paired with far smarter production and consumption of energy—from the chip, to the grid to the end user. This is where AI and climate investing converge. AI’s growth isn’t competing with climate solutions—it’s accelerating demand for them.

That convergence defined our work in 2025. In a year when venture fundraising fell to a 10-year low, we closed Fund III at $110M, more than doubling our assets under management. The fund enables us to make 25 new investments and follow-on investments to the strongest performers—technologies that are cheaper, faster, better. This year we added four new companies, made +13 follow-on investments, closed one exit, received two awards and hosted two major events. Bridge financings and founder resilience were defining themes as the market adjusted and our startups adapted, resulting in zero wind-downs in 2025. In Q4, momentum accelerated as three portfolio companies raised Series A rounds with new lead investors at meaningful markups (all to be announced soon)!

We’re heading into 2026 with continued conviction. The market for the technologies we invest in—those shaping the future of production and consumption—is large, growing, and increasingly unavoidable.

Howdy, Partner

What does it mean to “make Partner”? Venture capital firms, like law and accounting firms, have a Partner track. It’s a level that ambitious team members aspire to, reflecting hard work, shared values and

What does it mean to “make Partner”? Venture capital firms, like law and accounting firms, have a Partner track. It’s a level that ambitious team members aspire to, reflecting hard work, shared values and contributing to the firm’s success. At Active Impact, what it takes to become a Partner is something we’ve thought carefully about over the years, because it shapes who we hire, how we train and when we promote.

Our criteria starts with achieving competence in the five jobs we believe are essential to running a venture capital firm: raise capital, deploy capital, post-investment support, manage internal operations and manage external partnerships. We offer full exposure so every team member understands the whole system and how each part supports the rest.

But what truly sets someone apart is how they show up: with judgment, accountability and real ownership. Partners don’t just drive outcomes—they elevate others, and make decisions with the long-term health of the firm in mind. In short, Partners act like owners before they become owners.

We’ve also come to appreciate that strong partnerships aren’t built by duplicating the same skill set. Sophie has consistently exceeded the bar across the core work, and she brings distinctive strengths that make all of us better. Her leadership shows up in how we think, how we operate and the standard we hold ourselves to as a team.

It’s completely clear to Tom, Sam, and Mike that Active Impact is stronger because of Sophie. We’re proud and excited to welcome her into the partnership!

Dirty Deeds, Done Dirt Cheap

AI gets blamed for a lot these days—including higher power prices. But a new Lawrence Berkeley and Brattle Group study found the opposite: between 2019 and 2024,

AI gets blamed for a lot these days—including higher power prices. But a new Lawrence Berkeley and Brattle Group study found the opposite: between 2019 and 2024, states with rising electricity demand often saw lower prices. More demand spreads fixed grid costs over more megawatt-hours, while the real price drivers to date have been aging infrastructure, resilience investments and material inflation.

As investors and policymakers reframe overt climate mandates into talk of energy independence—and venture capital chases the next AI model—there’s an opening. The same exuberant build-out of AI infrastructure can accelerate the shift to a modern grid that supports more flexibility, and is increasingly powered by renewables and advanced storage.

Our aging grid needs investment, so prices will likely continue to climb in the years to come. But data centers, forecast engines and optimization tools can actually be a big part of the solution to rising retail electricity prices.

We continue to look for startups that could generate huge returns by meeting this rise in demand with the right tools that help upgrade our physical infrastructure better, faster and cheaper—while allowing for increased demand to be spread across rate payers (at the right times) that help keep rising electricity prices in check.

The Founder Games

We hosted our second Founder Summit in Vancouver, gathering 20 founders and senior leaders from across North America.

We hosted our second Founder Summit in Vancouver, gathering 20 founders and senior leaders from across North America. The morning featured sales coach Ryan Williams leading a practical workshop, but the sizzle emerged once the founders turned to each other. Again and again, the request we hear most from our portfolio is simple: connections with other founders.

The summit delivered exactly that—an open exchange of lessons on growth strategies, financing hacks, and operational playbooks, with insights flowing as freely across sectors as they did across dinner tables. We had founders sharing best practices on everything from Model Context Protocol (MCP) implementations to accelerated depreciation on single tenant leases.

A highlight for visitors was the bike ride around Stanley Park, which also included our partners from Deloitte Ventures, Dentons and RBCx.

The following week, Sam from our team joined Climate Week in New York. The conversations there had a different tone: fewer mentions of emissions or sustainability, more emphasis on AI, energy security and onshoring. But the central parallel was striking.

Our founder summit and New York Climate Week reminded us that behind the new language and shifting narratives, the goal remains the same: building durable businesses that make things people need, that move us toward a livable, sustainable planet and that make real economic sense for the end customer.

That combination—mission and market discipline—has always been the true edge of our founders. And in a noisy market, it’s also their most valuable resource.

AI of the Tiger

Investors are pouring money into AI startups with AI deals accounting for 71% of VC funding in Q1. It’s a goldrush.

Investors are pouring money into AI startups with AI deals accounting for 71% of VC funding in Q1. It’s a goldrush. The technology is reshaping white-collar work and accelerating at a staggering pace. But venture capital now faces a fork in the road:

Chase every potential power law winner, paying whatever it takes to avoid missing out.

Invest non-consensus, targeting differentiated returns by going where others won’t.

The surge in AI deals and valuations is unprecedented. To justify them, you have to believe in new markets, new revenue streams, and new venture math. For the elite few, that’s possible. For the rest, history tells us speculative bubbles eventually pop when results fail to match the capital inflows.

So where do we stand? We’ve built selective exposure to specialized, agentic AI that can accelerate climate solutions. But we’re putting all software investments through a tougher lens: do they unlock an entirely new growth paradigm, or are they easily disrupted by AI?

Meanwhile, climatetech is being rattled by U.S. policy headwinds. Many investors are backing away. We see this as a chance to make high-conviction, non-consensus bets on what the future will undeniably require (and that are hard to displace with AI).

In short: we’re long climate, with AI exposure where it strengthens the case.

Living in a material world, and Sophie is a (bio)material girl

We are thrilled to announce the final close of our Fund III at $110 million! For 18 months, our team has had thousands of meetings with a pipeline of hundreds of potential partners globally.

The chemical processes that underpin our modern world are overdue for disruption. From fuels and fertilizers to plastics and packaging, chemical manufacturing drives ~5% of global GHG emissions—more than double that of aviation. Despite its massive footprint, the industry has seen little innovation since the mid-20th century. But that’s changing. Advances in AI, synthetic biology, and industrial automation are opening the door to a $5 trillion materials market transformation—and we’re looking for the teams that will lead it.

In her latest thesis work, Sophie did a deep-dive into materials and the investible whitespace of biomanufacturing. By using engineered microbes to convert renewable feedstocks into high-value materials, biomanufacturing offers a credible path to decarbonize the products we rely on every day. Read Sophie’s article to explore the technical and commercial challenges to scaling this sector—and what it will take to unlock investable opportunities. As always, send exciting companies and founders our way!

BRIDGE OVER “TROUBLED?” WATER

We are thrilled to announce the final close of our Fund III at $110 million! For 18 months, our team has had thousands of meetings with a pipeline of hundreds of potential partners globally.

According to the latest data from Carta and also observed in our three fund portfolios, the number of bridge financings is extremely high compared to traditional up-rounds. But, not all bridges are created equal! As an investor, it’s important to understand exactly the kinds of bridges that your fund managers are getting you into (and avoiding). Here are just a few types that we have experienced in the last 12 months in this choppy market.

The underperformer - The company has failed to hit milestones due to poor management and needs money to stay alive. Strangely, many insiders will consider doing this but we generally avoid participating in these unless we are being defensive against highly punitive terms and success is at least still possible.

The changeover - The investors and management have a misalignment on goals or relationship and the bridge requires new money from new investors.

The market correction - The company has exceeded commercial milestones but investors have shied away from this space lately or valuations have dropped, but the insiders believe management is still capable of a big outcome.

The pre-emptive - The company has performed so well that the insiders set terms to increase their ownership through a super-pro-rata follow-on that saves the founder the effort of fundraising. We love these and have completed several in the past two years. The one drawback is that we are not allowed to mark them up in our books so some investors can misunderstand their value in the short term.

To make bridge rounds even more complicated, some are priced (shares) but many are SAFEs or convertible notes. They might have valuations that are either higher or lower than previous valuations, but the most common case is a flat round for the first three examples and an upround for the pre-emptive bridges. So next time you hear that a company did a bridge financing, ask a few questions to determine if you are disappointed or excited.

$110M Problems … but Closing Ain't One

We are thrilled to announce the final close of our Fund III at $110 million! For 18 months, our team has had thousands of meetings with a pipeline of hundreds of potential partners globally.

We are thrilled to announce the final close of our Fund III at $110 million! For 18 months, our team has had thousands of meetings with a pipeline of hundreds of potential partners globally. The fund was co-anchored by Northleaf, who joined as a new investor, and Fondaction, a returning major investor. Fund III is nearly double the size of Fund II and brings in much greater institutional backing with Boann, Co-operators Corporate Venture Capital Fund, Deloitte Ventures, InBC and others. We’re immensely grateful to the 53% of Fund III investors that are invested in prior funds, over half of which are investors in all three of our funds.

It is a difficult time to raise capital, but climate change doesn't care about market conditions or political cycles. Some VC's have delayed plans to raise new funds, and some that were previously deploying into climate have started to shy away. We are more bullish than ever on the opportunity climate tech holds—particularly in Canada.

Fund III will make 25 portfolio investments with the majority being based in Canada. Canada is emerging as one of the best places in the world to build a climate tech company. We have the essential ingredients for global leadership in climate innovation: world-class affordable talent, strong public support, effective policies like IRAP and SR&ED, and respected and stable leadership. Canada is also an increasingly attractive destination for elite talent through the Tech Talent Strategy work permit program and academic talent avoiding the US.

The seven companies Fund III has already invested in are off to the best collective start we’ve seen. Now that our fundraising efforts have wrapped, we are full throttle on finding the very best teams and ideas. We are searching for outstanding founders or operators that want to build a climate company. If you’ve been successful with another venture and you want to build something massive, we want to talk!

Almost Famous

Last spring the team from Viewpoint with Dennis Quaid reached out to us because they wanted to produce a segment on impact investing for public television. Impact and climate tech investing isn’t new, but it’s still niche.

Last spring the team from Viewpoint with Dennis Quaid reached out to us because they wanted to produce a segment on impact investing for public television. Impact and climate tech investing isn’t new, but it’s still niche. Most people (but not you, because you subscribe to this newsletter) don’t know that making money and creating environmental or social solutions at the same time is possible. The general public still silos doing ‘good’ with charity and doing ‘well’ (making money) with business.

We agreed to take on the project because we could feature one of our portfolio companies at the same time and demonstrate how this can be done. Future was an ideal choice because they are one of the few B2C companies in our portfolio with their FutureCard, the first Visa debit card that gives cashback rewards for sustainable choices (like public and electric transportation instead of gas purchases). Future illustrates our core investment thesis—that products that deliver cost savings for their customers while also achieving meaningful emissions reductions with no sacrifice in quality can yield outsized returns.

Having film crews in our North Vancouver office was unfamiliar territory for us, but worth the trouble if we succeed in reaching millions of views through hundreds of affiliate TV stations across the US and share the massive opportunity in climate tech venture capital. You can watch the segment here and critique our acting skills.

Ain’t no mountain high enough

Mike and Sam ventured to Africa last month to accomplish two big goals: visit our two portfolio companies operating in Africa and climb Mt. Kilimanjaro. The trip was a success and an experience of a lifetime.

Mike and Sam ventured to Africa last month to accomplish two big goals: visit our two portfolio companies operating in Africa and climb Mt. Kilimanjaro. The trip was a success and an experience of a lifetime.

We don’t invest in Africa often and so when we do, the bar is very high. These founders impressed us enough to invest and reminded us how special they are when we got a chance to visit their place of work. Jeff is building Jaza for the next 100 years and there is no personal sacrifice that has or will tamper his ambition. His company is structured with clear systems to allow scale without layers of supervision and a culture of pride and service. Michael is breaking product build records by going nights without sleep to build a one in a million brand called Zeno. He is charismatic and inspiring, always bringing new interest and excitement to the table with high quality employees, investors and customers that become advocates.

Jaza Energy is one of the first investments from Fund I that we exited last year. Over the course of our investment in Jaza, they provided four million solar charged batteries to families and businesses in rural Tanzania and Nigeria that don’t have access to electricity. Zeno is among our most recent investments from Fund III. Zeno’s electric motorbikes and battery swap infrastructure are replacing gas-powered bikes by being more affordable to buy and operate. Mike wrote an article about their experience, click here for the full version.

A rose by any other name…

Tom just returned from the Cleantech Forum in San Diego where a few key themes stood out. As expected, there was plenty of angst related to the early flurry of activity from the White House slowing climate tech momentum.

Tom just returned from the Cleantech Forum in San Diego where a few key themes stood out. As expected, there was plenty of angst related to the early flurry of activity from the White House slowing climate tech momentum. There was also bewilderment at the pace of innovation and technological advancement, highlighted by DeepSeek’s announcement of compute power that will result in using a fraction of the energy previously forecasted for data centres in support of the unstoppable march of AI.

The most thought provoking topic was a push to reframe language around climate tech businesses. Given that such businesses are in the crosshairs of current governments and anti-woke sentiment, let’s change the words we use! Instead of “cleantech” and “climate impact”, refer to “the energy transition”, “energy security” and “job creation”. Talk of unleashing national prosperity with homegrown innovation, cost reductions and products with greater efficiency that avoid pollution and keep our air and water clean. While it may seem disingenuous, language matters–and a simple reframe could help bridge polarized views on decarbonizing technologies.

Case in point, consider our portfolio company Jetson, highlighted in the Founder Spotlight below. Jetson could lead their sales pitch to customers by touting their impressive GHG reductions versus incumbent gas home heating or cooling, but it’s much more effective to lead with their heat pump installation and maintenance business being a cheaper, more efficient way to heat and cool your home—which just happens to make a sexy climate impact.

Later, litigator

Great lawyers don't just have a strong understanding of the law. In fact, drafting standard legal documents according to customer needs is already getting replaced by Al. What great lawyers do is much harder to replace.

Great lawyers don't just have a strong understanding of the law. In fact, drafting standard legal documents according to customer needs is already getting replaced by Al. What great lawyers do is much harder to replace. They are great project managers, effectively communicating and managing all stakeholders to a desired schedule. They are great at customer service, through responsiveness to calls and emails. They are great negotiators, working with you as a partner to ensure optimal outcomes on the highest risk and highest value aspects of the contract or deal. They are proactive, informing you on trends and offering access to their network. They are great estimators, telling you with a high degree of accuracy what something will cost. For most of my 30 year career I have been responsible for dealing with lawyers on behalf of my companies and I've been exposed to many bad lawyers who ran bad processes. But the great ones like Jason at Golbey Law, Ed and Laura at Osler and Chase at Dentons really stand out and have made me appreciate how valuable it is for founders to ensure they have a strong lawyer in their corner. The investment of time to find them will pay off in spades.

In the meantime, here are some of my lessons learned and tips for effective management of lawyers until you find one of the greats.

1) Lawyers work for you -I think sometimes founders are intimidated by lawyers and take their word as gospel since they are seen as experts or feel they have to wait patiently to hear back. Instead, keep in mind that this is your company and you know the things that are most important for you to accomplish in any contract or deal, even if those might be different than the legal advice you are getting. And unfortunately sometimes the squeaky wheel gets the grease so don't hesitate to assign or request deadlines when you need documents turned around quickly to meet your schedule.

2) If you don't know who the project manager is, it's you - often there are 5 or more parties at the table (a founder, current shareholders, a VC and legal counsel for both sides) and left unassigned I've seen all parties blame each other when a deal slips at the end of the process. Instead, try to reverse engineer every step that is required and assign a target date and owner for each of those steps and email that schedule out to get approval from all parties on the plan. Then simply email updates daily or weekly with what is ahead and behind schedule, who you are waiting for and what people need to prepare for next.

3) Pre-approved caps - Most of us have at one point been surprised by a big legal bill. To avoid this, you should ALWAYS get your lawyer to provide an estimate and then instruct them in writing that they do not have authorization to bill you above that cap without your permission to proceed. At least then it will be in your control to understand what is driving up the extra hours and if that is necessary.

4) After one set of revisions, get everyone on a call - sometimes the back and forth with the counsel for a big company will kill you with the death of 1000 cuts as each turnaround of docs creates another delay and adds more cost. A lawyer that is not motivated to get a deal done has nothing to gain by agreeing to any item that increases risk for their client. Instead, I have found it very effective after the first set of redlines and revisions to get the business stakeholders and lawyers from both sides in a meeting together to discuss in layman's terms what is acceptable to get the deal done. The business owners are often comfortable with reasonable risks and understand the nature of the project better, which gives the lawyers license to absolve themselves of certain blame and switch gears to just getting the legal language nailed down.

I Fought the Law (and the Law Won)

Write-offs are a necessary part of venture investing. They are unavoidable if you do enough investing for long enough and because of this, all venture funds build write-offs into their models to demonstrate how the winning companies can provide returns that both compensate for the losses and deliver high performing results as a portfolio.

Write-offs are a necessary part of venture investing. They are unavoidable if you do enough investing for long enough and because of this, all venture funds build write-offs into their models to demonstrate how the winning companies can provide returns that both compensate for the losses and deliver high performing results as a portfolio. But most venture funds write off their underperforming companies long before they are actual losses by not investing any more time in them, quietly removing them from their webpage and never discussing them publicly. At Active Impact, we are striving to be different. First, we promised founders that as long as they are willing to keep fighting, we will be in their corner fighting to the end (in fact, this is one of our core values). Second, we promised investors and our followers the highest levels of transparency which means that you can't just share the good news, you also have to share the bad. And, these setbacks are an opportunity to do a post-mortem and learn what we could try differently next time and to share these lessons. By the numbers, we have now invested in 37 companies, exited 7 of those and we just had our first write-off. So far, we are well above average on both exits and survival rates.

So here is a brief story about Anshula and the company she founded over 10 years ago called Sametrica. Anshula is a warrior and deserves a massive amount of respect. She entered into the impact and ESG measurement space before almost anyone else did–she knew the material better than most and built a strong MVP. She worked to serve and educate some of the largest brands while keeping her company alive for years with no additional funding, often by going without pay herself. Thank you Anshula for all that you did. We know that you exhausted every possible option to survive for as long as you could.

For our part, we got some things right and we got some wrong. We picked the ESG measurement market before most investors and it's now very large. We scored Anshula very high on tenacity which proved to be true. We declined follow-on financing even though our fund had capital reserved because our job is to concentrate capital in our top performing companies (Sametrica only received $250K from us 5 years ago, while our top companies have received 10% of the fund). Some things we got wrong were: insufficient diligence on the minimum financing required to achieve initial milestones, macro headwinds on ESG, and most importantly, gaps in the leadership team on product and sales. We have always believed that we can help founders hire what is missing, but we now believe that there is a minimum level of experience required on the team at the time of investment in a few core areas. These lessons are now documented as part of our learning catalogue and have changed the nature of our due diligence process for the last few years. We hope they have made us better investors.

Goodness Gracious, Great Balls of Fire

In Canada last year, more than 6500 fires burned across 18.5 million hectares of forested land, which released an estimated 0.5 gigatons of carbon dioxide into the atmosphere, the highest amount from a forest fire season on record.

In Canada last year, more than 6500 fires burned across 18.5 million hectares of forested land, which released an estimated 0.5 gigatons of carbon dioxide into the atmosphere, the highest amount from a forest fire season on record. Just a few weeks ago, massive and intense wildfires in Jasper National Park ravaged more than 32,500 hectares of landscape and devastated the historic town of Jasper. It’s not just an increase in media coverage – the reality is that wildfires are becoming more intense, frequent, and burning more land every year. The Canadian Interagency Forest Fire Center reports that between January and mid-July 2023, over 25 million acres of land burned in Canada – almost 30% more acreage than any annual burn in the last 40 years and almost 4X as large as the previous 10 year high.

Over the last few months, we’ve been diving deep into what we call the “Chain of Fire” – the various stages of a fire, and corresponding opportunities for fire management.

In our research, we found novel technologies across the value chain. Many of these focus on the stages of the Chain of Fire where a fire is already underway, like early detection and automated recommendations to reduce spread. This is certainly valuable – if we detect fires earlier, we can manage them and get them under control more effectively. However, there are other parts of this value chain that could yield outsized environmental impact and financial upside that aren’t yet served by as many innovative technologies. Specifically, the first and last links in the Chain of Fire: fire prevention through more effective forest management and ecosystem recovery after a fire are both pivotal areas in the chain of fire where we hope to see many more competitive solutions that make economic sense for customers. Much of the fire prevention and ecosystem recovery work that needs to be done relates to more effective planting and vegetation management across large swaths of land, unlocking interesting applications for robotics and AI.

To dive deeper in this issue and learn more about startups working to combat the spread of fire, you can check out Sam’s longform piece.

Risky Business

Last week, Mike, Qhalisa and Sam attended Climate Week in New York City - a week filled with events, relationship building with great partners and lessons learned.

Last week, Mike, Qhalisa and Sam attended Climate Week in New York City - a week filled with events, relationship building with great partners and lessons learned.

TL;DR - climate risk might be better portrayed as a risk to your current way of living - your home/coffee/wine/travel/skiing/appreciating nature/political stability will all be impacted. Humans have tended to be good at predicting the future by analyzing the past but in this case, we will have to be better at understanding what our already determined future climate is, so that we can focus on quickly adopting the available and already viable solutions.

We also wanted to share some key learnings from an event we co-hosted below:

1) A lot of value comes from intimate discussions with smart people that have different viewpoints. Our topic was electricity grid challenges resulting from the rise of AI’s energy consumption, and how AI could actually help navigate the surge in demand. While fundamental changes to the grid are required, many feel that the safety and dependability that our utilities provide must continue to be priority #1.

2) Several large utilities are feeling pressure from their Public Utility Commissions (PUC) to improve grid flexibility, which means less peaker plants, decreased emissions and more innovative ways to shift when people consume power. They are looking to adopt tools that can safely and reliably provide more visibility into decision making. There are several startups doing this well, such as ThinklabsAI in our portfolio.

3) The energy transition has an uncertain short-term outlook, but the long term looks very strong. Later stage investors, and those that invest in infrastructure, are cautiously deploying capital into solutions. They hope to see more first of a kind (FOAK) facilities successfully built and more evidence of strong outcomes for climate companies in public markets. Fortunately, we heard repeatedly that the significant risks for society need to be addressed urgently, and the corresponding upside for those that have strong solutions could be huge.

4) Recognition that the Active Impact Investments brand is growing globally. Over the course of the week, we had people from around the world congratulate us on progress, exits, fundraising and share their excitement for our new investments. Our event only had space for 25 people and ended up with over 700 people registered! In VC, brand matters, and it was nice to see peers recognize the work we’re doing on both sides of the border to help move the needle on climate change.

I tried to make a joke about measuring, but it was too short

Active Impact entered the market at a time when there was a huge gap at the seed stage in climate funding, where we felt our skills were particularly well suited to help. Since the beginning, we have been searching for solutions that will create the most positive impact moving forward.

Active Impact entered the market at a time when there was a huge gap at the seed stage in climate funding, where we felt our skills were particularly well suited to help. Since the beginning, we have been searching for solutions that will create the most positive impact moving forward. Our mission is to “provide funding and talent to accelerate the growth of early-stage companies to achieve venture scale profit, while solving the most urgent environmental issues.” To evaluate our success, we measure our progress on impact in addition to financial metrics. Earlier this year, we proudly celebrated 1M tonnes of GHG emissions averted via our portfolio companies.

But after we spoke to much larger funding entities, we began to rethink how we represent our impact and decided to update our ‘Theory of Change’. We now also measure progress using a metric of emissions reductions per dollar of revenue. We realized that if you simply look for the highest GHG emissions reductions realized during the investment period, then you could invest in a single late stage company and immediately claim 1M tonnes of emissions averted. However, our assertion is that this pales in comparison to the potential within the 37 investments we have made so far. We believe the compounding effect of the growth of our portfolio companies will lead to cumulative GHG reductions far beyond 1M tonnes. We challenge others looking to maximize impact to consider a similar approach, and get comfortable with the fact that the highest total volume of emissions reductions may happen after your investment period.

Walk this way, talk this way … like this

“We Put Founders First”. There were several situations over the course of the last month where we had an opportunity to put this core value into practice. While it takes a little more time and thought, we think it's worth the effort.

“We Put Founders First”. There were several situations over the course of the last month where we had an opportunity to put this core value into practice. While it takes a little more time and thought, we think it's worth the effort:

It's important that founders we partner with have similar values to us, and that we build this alignment early on. When we write a term sheet to lead a new deal (as we did this past month), we don’t just send a legal doc, we include language that encapsulates our brand, shares our values and discusses how we like to partner with founders.

There can be incredible value in post-investment support. We onboarded two new portfolio companies in July, done not with an email saying ‘welcome aboard’ but with a meeting where all 10 members of our team introduced themselves and shared how they can provide support. We lean in every month in coaching calls to help with sales, hiring, fundraising and any other thing that is needed.

We like to celebrate wins. Last month we added our newest process to recognize our founders with exits, not with a bottle of champagne but with a custom award citing the things they did best, accompanied by a personal letter expressing what we admired about our time working together.

It’s much easier if you only deploy capital, it’s hard to build lifelong relationships and a brand that stands out.

Scoring a “Tofurkey”!

That is the question. We are doing our next close on June 15 and we have several institutional entities that are in due diligence (DD). At this point, "maybes" are tough (there are over 300 of you!). "Yeses" are great as they reduce our time in market and "nos" are helpful as they allow us to prioritize our time for investors that still have questions.

Any bowler out there knows that scoring 3 strikes in a row is called a “Turkey”. Well, what do you call it when a climate fund announces 3 exits in a week? Maybe a “Tofurkey” since the carbon footprint is lower?

With just 32 investments in our first two funds, we had the great honour and pleasure of announcing 3 exits in the second last week of June. Now, there is some fineprint here. The Sustain.Life and Pantree exits officially closed during that week, and Keela closed a while ago but we were waiting to make a coordinated announcement with their acquirer. Similarly, Pantree’s buyer requested that exit details are not shared on social media. In a time when many investors and LPs are looking for liquidity/DPI, we are happy to share this good news and lock in some returns. And of course, we are thrilled for our founders, who were able to execute on a plan that secures the long term funding needed for their businesses to continue scaling. We feel our biggest potential winners are still operating in the portfolio so there is still much work to be done.

Dilly of a Pickle for the Green Transition

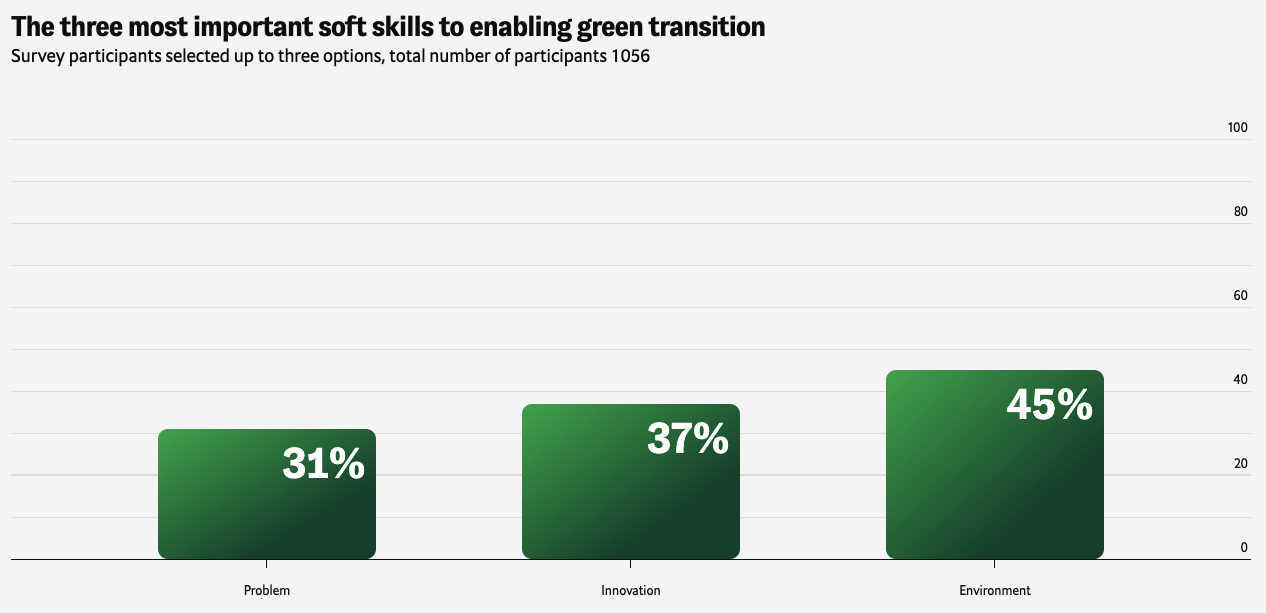

Drastically reducing GHG emissions demands a massive economic shift–across industries, geographies and roles. The problem may seem insurmountable, but we know that every challenge comes with opportunity. To seize it, we need the right people working to keep our planet inhabitable.

Drastically reducing GHG emissions demands a massive economic shift–across industries, geographies and roles. The problem may seem insurmountable, but we know that every challenge comes with opportunity. To seize it, we need the right people working to keep our planet inhabitable.

This is easier said than done. Globally, hiring slowed between 2022 and 2023, but climate-related roles bucked the trend. The share of green talent in the workforce rose by 12.3% across 48 countries. The jobs requiring green skills grew by 22.4%, but here’s the thing: only one in eight workers in the market have these skills. We need to address the supply and demand issue, which will require a multi-pronged approach to upskill and reskill people from legacy industries to green jobs. For example, the percentage of auto workers that need EV skills rose to 61% in 2023. The Conference Board of Canada predicts that just one year of training can enable a green transition for 99.7% of high risk, low mobility workers, such as those in oil and gas jobs.

With a growing "green skill" shortage, choosing top talent within climate tech is increasingly important. While many choose to hire based on experience, we work with founders to go beyond experience and hire for high potential. We work with our portfolio companies to identify a candidate’s ability to adapt and learn, problem solve, take accountability consistently and most importantly, align with the mission of an organization. If you're a high potential candidate with a passion for climate tech please reach out. We'd love to get you into the right role within our portfolio!

DD, or not to be…

That is the question. We are doing our next close on June 15 and we have several institutional entities that are in due diligence (DD). At this point, "maybes" are tough (there are over 300 of you!). "Yeses" are great as they reduce our time in market and "nos" are helpful as they allow us to prioritize our time for investors that still have questions.

That is the question. We are doing our next close soon and we have several institutional entities that are in due diligence (DD). At this point, "maybes" are tough (there are over 300 of you!). "Yeses" are great as they reduce our time in market and "nos" are helpful as they allow us to prioritize our time for investors that still have questions. Please reach out and let us know what you need.

If you are a capital allocator, you might wonder why fund managers are pushing for a faster timeline and looking to increase committed capital to a fund (including us, sorry for all the emails). Here's our take, worded simply from our perspective at this moment in time. On amount, we already have enough money to run our third fund. But we are seeing a lot of amazing, well-timed climate deals that we want to take large ownership stakes in and we have incredible talent pounding down our door to work with us–so the only constraint is access to capital. On timing, fundraising is the only thing we do that doesn't serve our current investors or founders. It takes time away from deal sourcing, picking winners and providing post investment support. Those are the things that drive our returns and impact, so we try hard to contain fundraising into short periods once every 3-4 years.

We're grateful to have had success with our Fund III raise so far. Now it's the most important part–time to finish strong. If you’re interested in what we do, take a few minutes in the coming days to look through our data room and get to know us better. If you don’t have access, let us know and we can share it with you. With our Fund II companies growing quickly and our first two investments out of Fund III under our belt, we're ready to direct 100% of our attention towards creating the fastest growth possible for climate positive solutions.